February 2026 Property Market Update: RBA Rate Rise, Home Loan Impact & What It Means for Buyers

It’s been a busy few weeks in the property world.

At its first meeting of 2026, the Reserve Bank of Australia (RBA) increased the cash rate for the first time since November 2023. Even so, property prices have continued to climb in several markets and housing confidence has held up.

For homeowners and buyers in Wollongong and across the Illawarra, this latest rate move is particularly relevant. Shifting interest rates, APRA’s new lending rules and rising property values may influence borrowing capacity, refinancing opportunities and purchasing timelines in 2026.

Whether you're reviewing your home loan or preparing to buy, understanding the landscape early can put you in a stronger position.

Interest Rate News: RBA Raises Cash Rate to 3.85%

At its first meeting for 2026, the RBA lifted the cash rate by 0.25 percentage points to 3.85%, in response to rising inflation data.

This marked the end of the shortest rate-cutting cycle in the RBA’s modern history, following three cash rate reductions in February, May and August last year.

Inflation remains above target

CPI rose 3.8% in the 12 months to December (up from 3.4% in November).

Trimmed mean inflation was 3.3%, slightly up from 3.2%.

The RBA wants inflation “sustainably” within its 2–3% target band, ideally around the midpoint.

RBA Governor Michele Bullock said:

“The recent run of data gives the board a clear enough view that underlying inflation is too strong.”

All four major banks have confirmed they will pass on the increase.

According to Roy Morgan data, this 0.25% rise could add around $115 per month to repayments on an average $694,000 mortgage, pushing approximately 1.3 million households closer to mortgage stress.

If you're unsure whether your lender is increasing your rate, or how this affects your repayments, we can review your loan and compare it against the wider market.

The next RBA announcement will be on 17 March, and there is growing speculation that further increases may follow.

What Does the February 2026 Rate Rise Mean for Wollongong Homeowners?

For local homeowners, the key impacts may include:

Higher monthly repayments

Reduced borrowing capacity

Increased pressure on serviceability assessments

Greater importance of competitive loan pricing

With lenders competing aggressively for quality borrowers, refinancing opportunities may still exist — even in a rising rate environment.

If it’s been more than 12–18 months since your last review, a home loan health check may uncover savings or better loan features.

How APRA’s New Debt-to-Income Cap Affects Borrowers in 2026

From 1 February, APRA introduced new lending limits.

Banks can now issue no more than 20% of new home loans to borrowers with a debt-to-income (DTI) ratio of six or more. The cap applies separately to:

Owner-occupiers

Investors

This doesn’t mean high-DTI borrowers can’t get approved — but lenders will be more selective.

For borrowers in Wollongong and the Illawarra, this means preparation is more important than ever. Understanding your income position, expenses and borrowing power early can prevent delays.

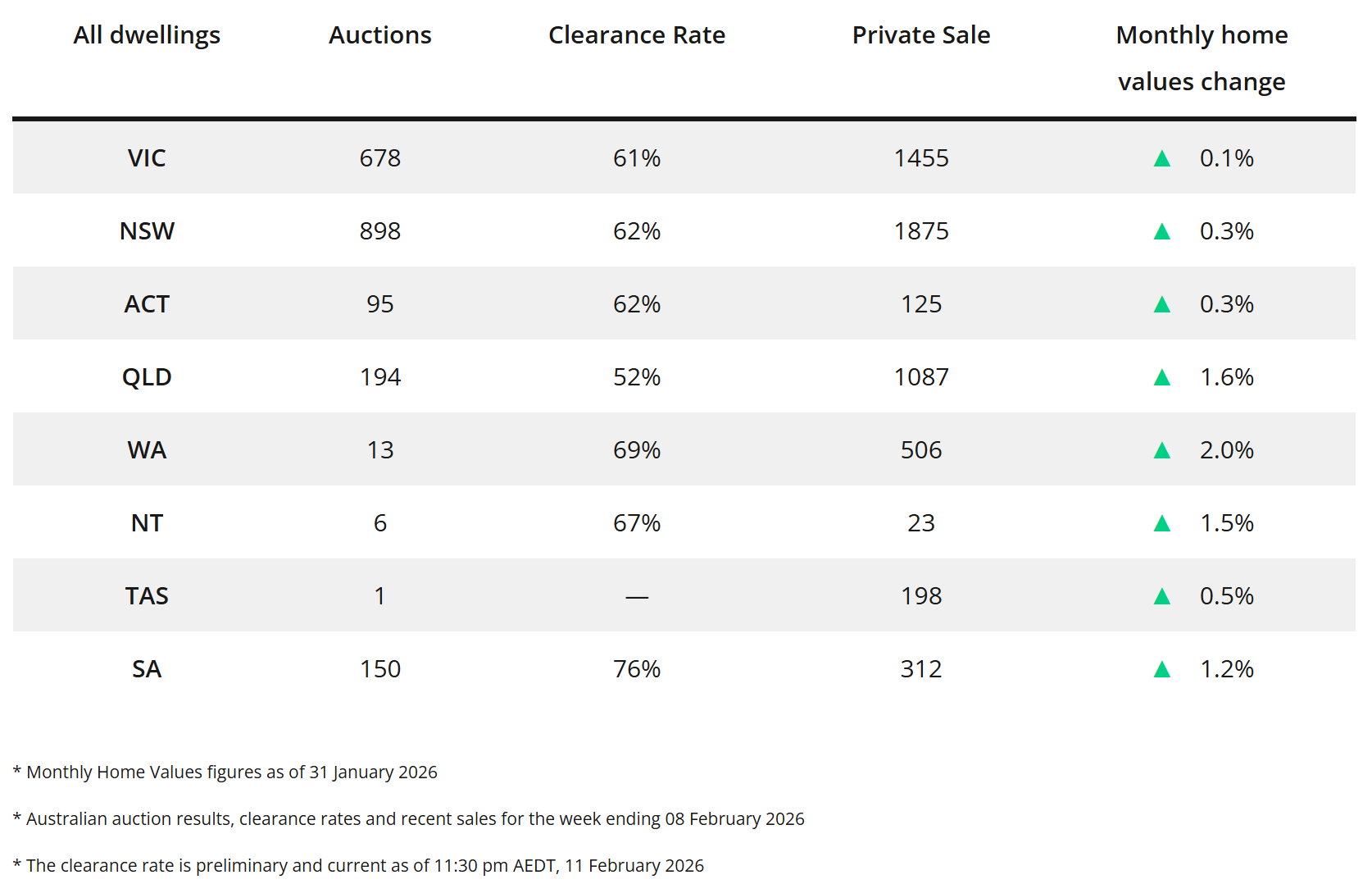

Home Value Movements: Prices Still Climbing

Regional markets also performed strongly, with combined regional values up 1%.

Despite affordability pressures and rising rates, demand remains supported by low inventory levels and ongoing housing shortages.

However, growth momentum is expected to moderate through 2026 as affordability and serviceability constraints weigh on demand.

Should You Refinance or Buy in 2026?

With interest rates trending higher, now may be a strategic time to:

Review your current interest rate

Compare lender offers

Consider refinancing

Assess borrowing capacity before further changes

Secure pre-approval if planning to buy

For buyers in Wollongong, acting early in 2026 may help you understand how lending changes affect your purchasing power before market conditions shift again.

Looking for a Mortgage Broker in Wollongong?

If you’re:

Concerned about rising repayments

Considering refinancing

Planning to buy your first home

Looking to invest

Unsure how APRA changes affect you

We can help.

As a mortgage broker, we compare lenders, assess your borrowing capacity and guide you through your options clearly and confidently. We cam assist client Australia wide. Early finance planning can make a significant difference in 2026.

Get in touch today to review your home loan or organise pre-approval.