April Market Update

With interest rates continuing to shift and property markets moving at different speeds across Australia, many borrowers are starting to reassess their position.

For homeowners and buyers across Wollongong and the Illawarra, this isn’t just headline news, it directly impacts borrowing power, repayments, and long-term strategy.

So what’s actually happening, and what does it mean for your next move?

Interest Rates: Pressure Still Building

Inflation is showing early signs of easing, with CPI rising 3.7% over the year to February. However, underlying inflation remains steady at 3.3%, which is still above the Reserve Bank of Australia’s target range.

Following the recent decision to lift the cash rate to 4.10%, lenders have passed on the increase in full.

There’s growing expectation that further rate rises could follow, particularly with global energy pressures adding upward risk to inflation.

To put that into perspective:

A $500,000 home loan could see repayments increase by around $239 per month

A $1 million home loan could rise by approximately $478 per month

For many households, that’s a meaningful shift in cash flow.

This is where working with a mortgage broker becomes valuable, understanding how these changes affect your specific loan structure, not just the headline rate.

Property Market Snapshot

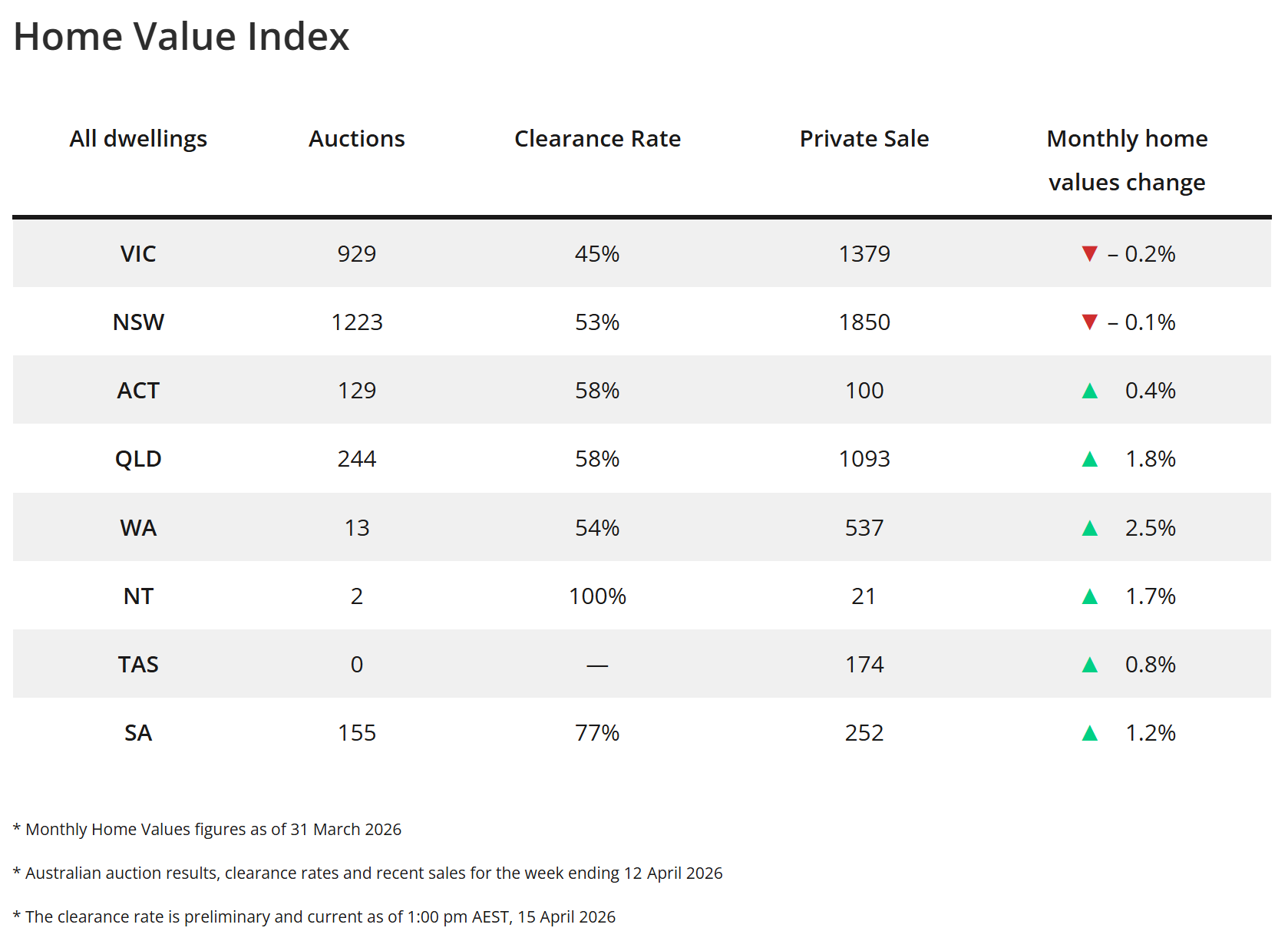

The latest Home Value Index highlights just how varied the market is right now.

NSW and VIC are seeing slight monthly declines

Queensland, WA and SA continue to show strong growth

Auction clearance rates remain mixed, reflecting changing buyer confidence

This reinforces a key point, there is no single “Australian property market” right now. It’s a series of micro-markets moving at different speeds.

What This Means for Borrowers

While national trends matter, your strategy should always be local and tailored.

As a mortgage broker, we’re seeing three key themes emerge:

Buyers have more opportunity

Softer conditions in Sydney are creating flow-on effects, giving Illawarra buyers slightly more negotiating power and time to make decisions.Repayment pressure is real

With rates rising, many borrowers are feeling the impact. A structured review of your home loan Wollongong can often uncover ways to improve cash flow.Strategy matters more than ever

In a fragmented market, the right loan structure and lender policy can make a significant difference to your outcome.

Should You Review Your Home Loan?

If your loan hasn’t been reviewed in the past 12–18 months, there’s a strong chance your current rate or structure may no longer be aligned with your goals.

A review doesn’t automatically mean refinancing. It means:

Understanding your current position

Comparing what’s available in the market

Making informed decisions based on today’s lending environment

This is where a home loan broker Wollongong can bring clarity and direction.

The Bottom Line

This market isn’t about reacting, it’s about positioning.

Whether you’re buying, refinancing, or planning ahead, having the right strategy in place can make a meaningful difference to both your cash flow and long-term financial outcomes.

Thinking About Your Next Move?

If you’re based in Wollongong or the Illawarra and want clarity on your options, we’re here to help.

We can:

Review your current loan

Compare lenders and rates

Structure your lending to suit your goals

Reach out to start a conversation around your next step.

Additional sources

Cotality Data Daily Home Value Index: Monthly Values

https://www.cotality.com/au/our-data/auction-results

https://www.realestate.com.au/auction-results/